Forecasting Housing Prices using Regimes and Weighted Ensembles

Using supervised, and unsupervised machine learning to forecast monthly median sale prices in Washington County OR.

Using supervised, and unsupervised machine learning to forecast monthly median sale prices in Washington County OR.

Utilizing ML in traditional cointegrated spread trading of cryptocurrencies.

Predicting stock movement via composition monte carlo based on historical earnings moves.

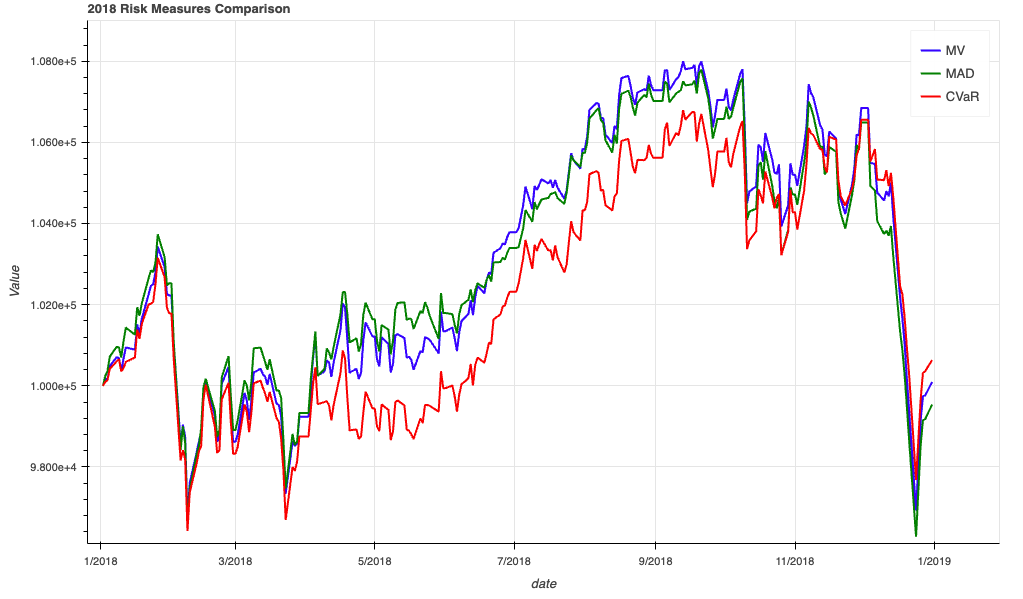

Backtesting portfolios constructed through Mean-Variance, Mean Absolute Deviation, and CVaR

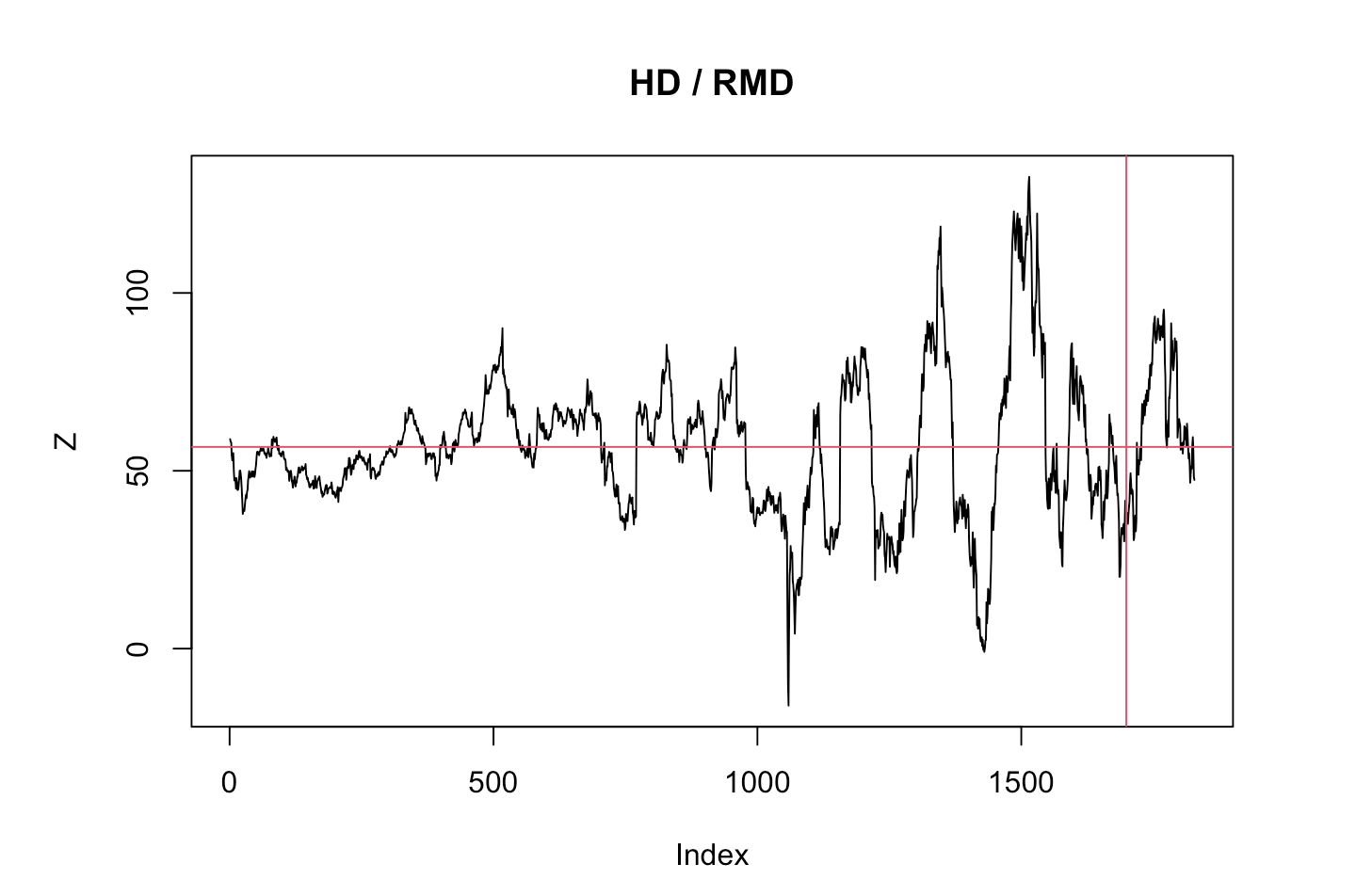

Using the Two-Step method in finding possible statistical arbitrage opportunities in the S&P500

Monte Carlo price forecasting using Normal vs Laplace distribution on historical pricing data.

Building a frame work on the research side to test which parameters are important when constructing a portfolio.

Looking at the supposed volatility smile in equities

Building a script that finds a quantitative hedge to your current positions

Qualitative search of over/under extensions of and within sectors

Lagrangian Mechanics Description of an Economic System